.png)

Personal income tax is progressive: the more you earn, the higher the applicable tax rate. A person's total income (salaries, investments, etc.) is taxed, after subtracting allowable deductions and bonuses.

Personal deductions:

Since the fall of 2022, the government froze personal relief and tax tranches until April 2028, which was confirmed again in the 2024 Fall Budget. This means that, even though incomes may increase with inflation, more people could switch to paying taxes or entering higher brackets.

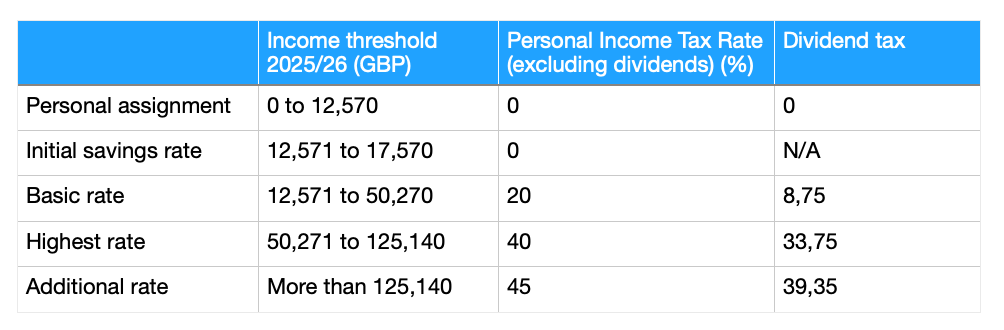

The rates for taxpayers resident in England, Wales or Northern Ireland are as follows:

The initial rate of 0% applies only to savings income. If non-savings income exceeds this limit, the initial 0% rate will not apply.

A dividend deduction applies to the first 500 GBP of an individual's dividend income. This deduction works with a 0% tax rate. Note that this does not apply to dividends on shares in an Individual Savings Account.

The dividend deduction does not reduce total income for tax purposes. Dividend income that falls within the deduction is counted for the limits of the individual's basic and upper tax rates.

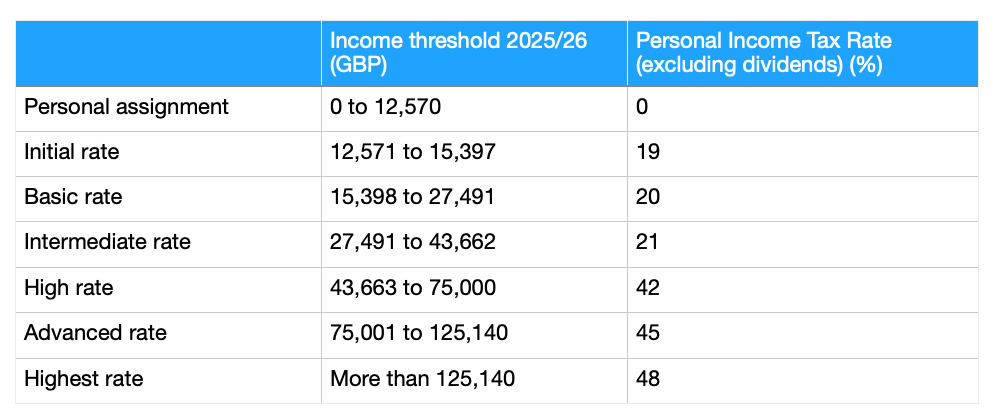

People resident in Scotland pay tax on income from work, pensions and most other taxable income, except dividends and savings, which are taxed at the rates indicated above, as in the rest of the United Kingdom.

The types of personal income tax in Scotland are as follows:

The taxation of trustees in the United Kingdom varies depending on the type of trust in question. In the case of accumulation or discretionary trusts, the first 500 GBP of income are taxed at a reduced rate: 8.75% for dividends and 20% for other types of income. Once this threshold is exceeded, a higher burden applies: 39.35% for dividends and 45% for other income.

When it comes to interest in possession trusts, trustees are taxed at 8.75% on dividends and 20% on other income. However, these incomes are usually considered directly allocated to the beneficiary, who must declare and tax them on their own income tax return.

It is important to note that trustees cannot benefit from the dividend deduction, which is available to individuals.

There are also special rules for other categories of trusts, such as trusts for non-residents, those with the interest of the trustor, or those established for vulnerable people. Given the complexity of this area, it is highly recommended to seek specialized advice in case of managing or setting up this type of structure.

Since April 6, 2025, the concept of domicile ceased to be relevant for determining the tax base in the United Kingdom. A new regime focused on fiscal residence was introduced, with transitional measures.

Income and Income Tax

Individuals who have been tax residents in the United Kingdom for more than 4 tax years (depending on Statutory Residence Test - SRT) are taxed on your worldwide income and profits, regardless of your previous address.

Inheritance Tax

New regime for newcomers

It is available to those who were not tax residents in the previous 10 years. You are exempt from tax on foreign income and earnings for the first 4 years of residence. It is mandatory to declare to HMRC the sums excluded under this regime.

Exemption for working hours abroad

It applies to income from employment outside the UK for the first 4 years of residence.

Transitional measures for non-domiciled persons

Temporary Repatriation Mechanism: allows bringing foreign incomes/profits prior to 6/4/2025 to the United Kingdom with reduced taxation:

Foreign assets held on 5/4/2017 and sold after 6/4/2025 will be valued at their market price of 6/4/2017 if certain requirements were met.

Trusts

If the trustor is a long-term resident, offshore trusts may also be subject to British inheritance tax.

The 2017 “trust protections” are eliminated: non-resident trusts may be subject to income/income taxes if the trustor is a resident of the United Kingdom and does not qualify for income and capital gains earned abroad.

Other points

The Business Investment Relief (BIR) is still available for investments made with foreign incomes/profits prior to 6/4/2025 through 5/4/2028.

Some agreements to avoid double taxation (India, Pakistan) continue to use the concept of domicile for inheritance tax.

Global incomes and profits:

Remittance regime:

Until April 5, 2025, the UK tax system allowed people who lived in the country but were not domiciled in it (called non-doms) take advantage of a special tax regime known as the tax base for remittances. This meant that they were only taxed in the United Kingdom on income and profits generated abroad if they were transferred to the country. However, this regime ceased to be available as of April 6, 2025, giving way to a system based exclusively on tax residence.

Domicile in the United Kingdom does not refer to nationality or usual residence, but rather to the country that a person considers their permanent home. It is a common law concept and can change over time. For example, someone may be born with one address in the United Kingdom (called home address), but acquire another if they settle in another country with the intention of staying there indefinitely.

In addition, there was the concept of presumed domicile, which applied to those who had been tax residents in the United Kingdom for at least 15 of the last 20 years. In these cases, they were considered to be domiciled for all tax purposes, losing the benefit of the remittance regime.

Until April 2025, the Non-Doms they could choose to pay taxes on a remittance basis each year, provided that they met certain requirements:

It should be noted that those who formally applied for this regime waived the personal income tax deduction and the annual exemption from capital gains tax.

A remittance involved more than transferring money to the UK from abroad. It also included situations such as:

Since this tax treatment could involve significant burdens, it was advisable to organize finances and accounts in advance before moving to the United Kingdom.

As of this date, the remittance regime was completely abolished. Now, the tax obligation in the United Kingdom is determined solely on the basis of residence, regardless of whether or not a person is resident in the country. Although some elements of the concept of domicile may continue to be relevant in certain transitional provisions, it is no longer the main criterion for establishing the tax burden.

In the United Kingdom, there is no alternative minimum tax (AMT).

This means that there is no parallel income tax system designed to ensure that taxpayers — especially those with high incomes and significant deductions — pay at least a minimum level of tax, as is the case in countries like the United States.

Instead, the United Kingdom bases its tax system on progressive rates, limited personal deductions, and a set of specific rules that limit the possibilities of excessively reducing the tax burden through exemptions or deductions.

Children under 18 are taxed independently, meaning they are responsible for paying taxes on their own income, just like adults.

However, there is an important exception when a child's income comes from donations made by their parents:

There are no local income taxes in the UK

.png)